Over the last two decades, India has seen a big push towards financial inclusion. Having a bank account can be the first step, allowing account-holders to receive welfare benefits, save, borrow and invest.

There are now nearly 2.6 billion bank accounts held by individuals in India, as reported by banks.[1] These numbers can include multiple accounts held by the same person, but exclude institutional accounts such as those owned by corporations or trusts.

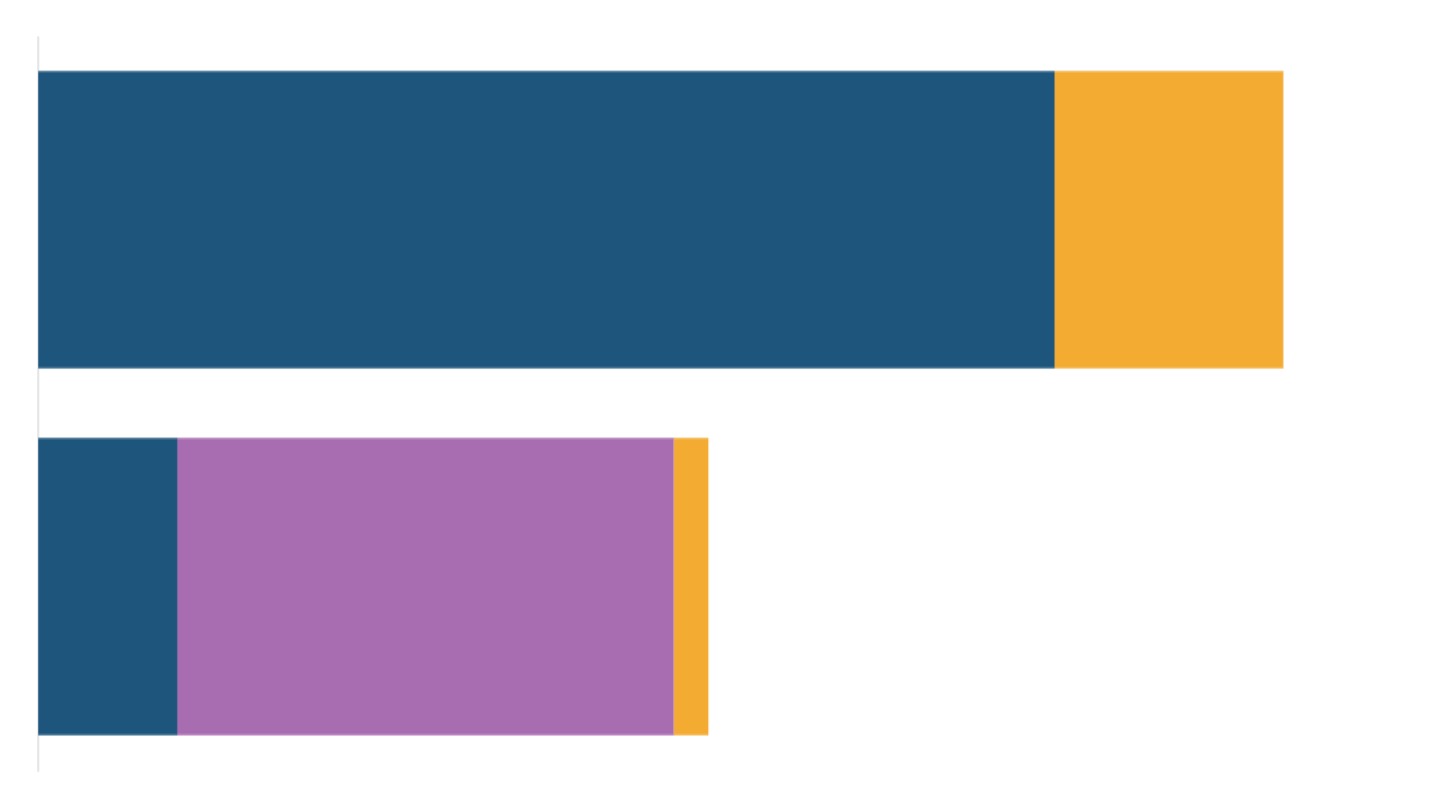

Indian men hold 50% more bank accounts than women.

Bank account penetration

Nearly every Indian household now has a bank account.

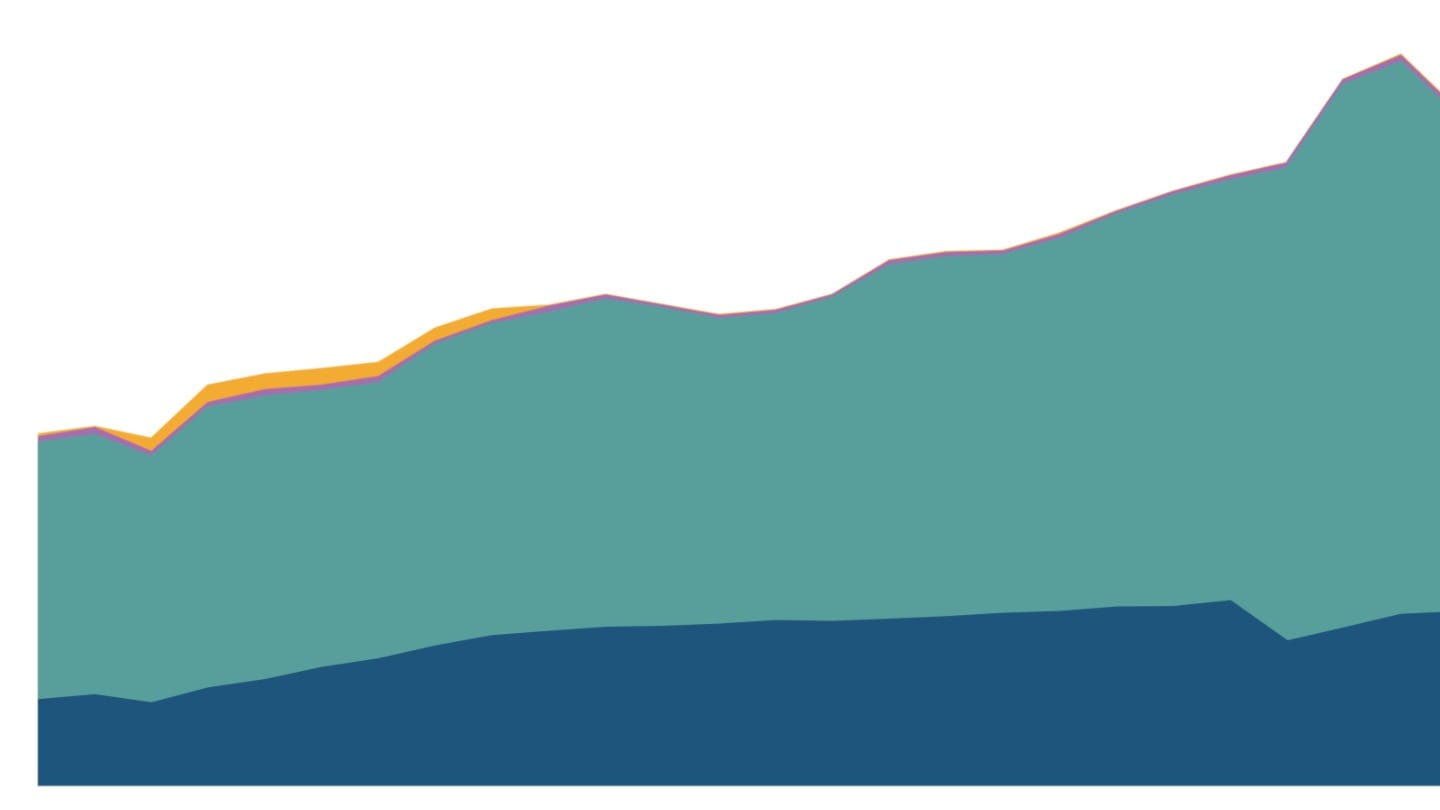

India's National Family Health Surveys have since 2006 recorded if the surveyed households had at least one member with an account with a financial institution such as a commercial or cooperative bank, or a post office. They find that from fewer than half of Indian households having a bank account in 2006, 96% of households had a bank account by 2021.

Even at the individual level, over nine in ten adult Indians now report having a bank account.[2] Access to a bank account is high across income groups; even among the poorest 20% of Indians, nine in ten now have a bank account.[3]

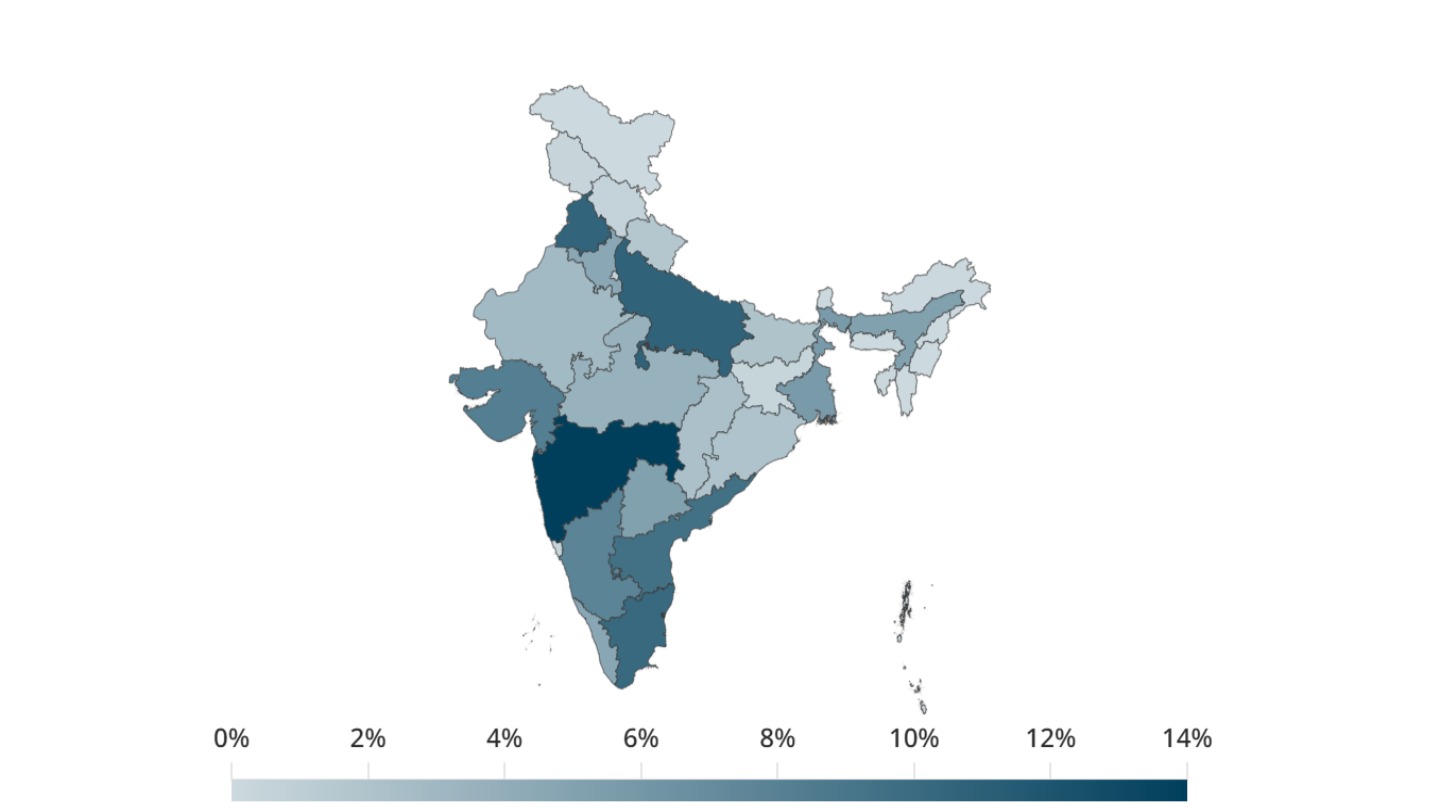

While banking access is widespread across the country, there are gender gaps in some states. The share of men with a bank account is more than 95% in most states, but is below 90% for women in several states. Relatively more developed states including Gujarat and Maharashtra, northern states and states in the northeast still have a gender gap in banking access.

Bank account usage

Despite most adults now having a bank account, the extent of usage could still have some way to go. By surveying a representative sample of 3,000 Indians, the World Bank's Global Findex Database 2025 found that about one-sixth of account-holders in India had an inactive account in 2024, meaning that they had made neither deposits nor withdrawals, nor had any incoming or outgoing digital payments in the preceding year.[4] Not having enough money in the account, distance to the bank, and lack of trust with the banking system were reported to be the key reasons Indians did not use their bank account. The share of inactive users was far higher in India than in the other surveyed developing economies. While the share of account holders with an inactive account in India was 16%, the average of low- and middle-income-countries was 4% in 2024.[5]

Women were more likely to be holding inactive bank accounts. About 20% of female account owners in India were found to be having inactive accounts compared to 12% among male account owners. This gender gap was particularly large in India, the survey found.

[1] Basic Statistical Returns of Commercial Banks, Database on Indian Economy, Reserve Bank of India.

[2] The Comprehensive Annual Modular Survey conducted by the National Statistics Office in 2023 asked individuals whether they had "an account individually or jointly in any bank/ other financial institution/ mobile money service provider".

[3] Among the poorest 20% of adults, 89% of women and 94% of men had a bank account in 2023. The proportions were 93% for women and 98% for men in the richest quintile. Quintiles are created by arranging the adult population in ascending order of monthly per capita consumption expenditure, and dividing into five equal sized groups.

[4] Klapper, Leora, Dorothe Singer, Laura Starita, and Alexandra Norris (2025), "The Global Findex Database 2025: Connectivity and Financial Inclusion in the Digital Economy", Washington, DC, World Bank. The 2025 survey was conducted with 140,000 people above the age of 15 residing in 141 countries by Gallup, Inc. as a part of the Gallup World Poll. Samples in each country are nationally representative.

[5] Klapper, Leora, Dorothe Singer, Laura Starita, and Alexandra Norris (2025), "The Global Findex Database 2025: Connectivity and Financial Inclusion in the Digital Economy", Washington, DC, World Bank.